Published on 13 May 2020

The Chief Executive of Hong Kong SAR Government has announced on 12 May 2020 about details of the procedures and documentation requirements for application of the subsidy under Employment Support Scheme (ESS) as follows:

Application procedures

The employers can apply for the subsidy by lodging the application as per the following procedures:

- The employer is required to lodge the application of subsidy by completion and submission of the application form online (website for application of the subsidy will be published by the Government soon#);

- The employer is not required to submit any records of MPF/ORSO contributions made for their employees during the application. The employer just needs to authorise the appointed MPF/ORSO trustee to release the records of MPF/ORSO contributions made for the employees to the Government directly;

- The employer is not required to pay any charges for the application. All the administrative charges arising from the application to be levied by the MPF/ORSO trustee, will be borne by the Government.

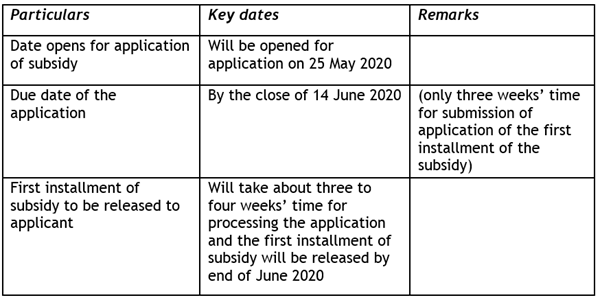

Please also pay attention to the below timelines for application and release of first installment of subsidy as follows:

# Please note that the relevant website for application of the subsidy will be announced by the Government within next week. Once we receive any updates, we will inform you immediately.

Further updates from the government

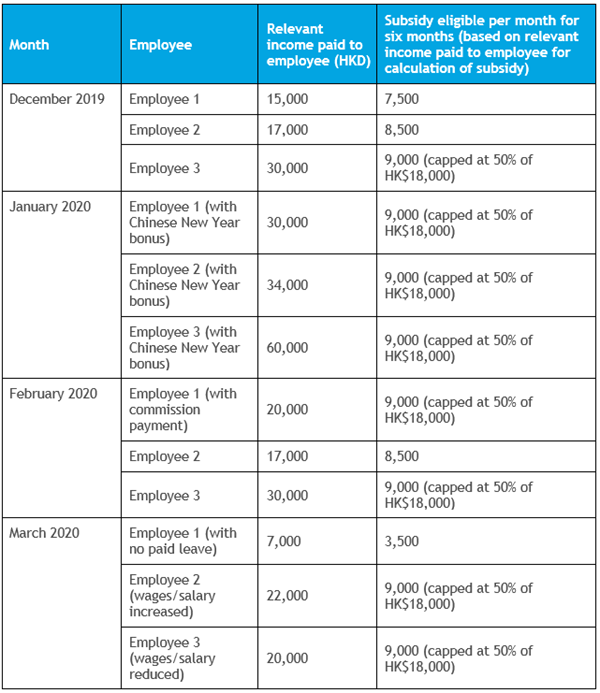

1. Consideration of payroll and headcount of a specified month for calculation of subsidy

The latest announcement made by the Chief Executive and the Secretary for Labour and Welfare confirmed that the employers can choose payroll amount of any one month from December 2019 to March 2020 for the basis of calculation of the subsidy. However, the headcount will be measured against the employer's headcount as per MPF/ORSO contribution record in March 2020 (that means the employers cannot choose the headcount size of any one month in December 2019, January and February 2020). The table below sets out the examples of the calculation of subsidy in a particular month for your reference.

- In the above example, January 2020 payroll would be chosen as the specified month for application of the subsidy and the headcount size of three employees as of March 2020 must be maintained in the period from June to November 2020.

- Payment of subsidy for June, July and August 2020 will be calculated on the basis of the relevant income paid to employees in the specified month.

Enhancements of the eligibility of the subsidy under ESS

a. The subsidy now also covers for employees whose age have reached 65 or above and employers are making MPF voluntary contribution for them in March 2020.

b. The employees of construction and catering sectors (such as workers, engineers working at construction sites for construction and consulting companies, chefs of food producers who have previously excluded from the category of 'regular staff' eligible for the application of subsidy under ESS, are now included).

c. The application for the first installment of subsidy will cover for employees who have already set up their MPF account with the MPF trustees on or before as at 31 March 2020 (excluding backdating). For those employees whose MPF account set up after 31 March 2020, the employers can apply for the subsidy for them when the second installment of the subsidy opens for application.

d. Self-employed persons who have set up an active MPF account on or before as at 31 March 2020 (excluding backdating) and with that account remaining opened as at 31 March 2020 will be eligible for an one-off subsidy of HK$7,500.

2. Proposed timeline for releasing the subsidy to employers

The subsidy will be disbursed in two installments, with the first installment of subsidy to be released by end of June 2020. The first installment of subsidy will cover salaries for the months of June, July and August 2020. The second installment of the subsidy will be released in September for covering salaries for September, October and November 2020 (details of the application procedures and timeline will be announced by the Government later).

3. Employers' undertaking

For receipt of the subsidy under ESS, employers must give two undertakings to the government (the actual wording of the declaration of the undertakings is yet to be confirmed):

- the subsidy must be 100% used to pay employees' salaries; and

- March 2020 headcount must be maintained throughout the period from June to November 2020 when the two installments of subsidy payments will be released by the Hong Kong Government respectively.

The Secretary for Labour and Welfare Law Chi-kwong emphasised that the employers have to maintain the number of employees with MPF/ORSO contributions as of March 2020 in the period of June to November 2020 as one of the undertakings for the application of the subsidy. For instance, if an employer had 40 employees in March 2020 but only 30 in June 2020 due to termination/resignation (not redundancy) of employees, it must further hire ten employees in June to fulfil the undertaking.

Upon receipt of the first installment of subsidy, the employer has to sign a declaration to undertake not to redundant their employees and have to use 100% of the subsidy to pay employee' salaries.

4.Penalties

If there is any reduction in headcount during the subsidy period compared to March 2020 or if the subsidy is not 100% used to pay employees' salaries, the government would adjust the subsidy with claw-back in whole or in part from the employer and the employer may be subject to penalties (formula of claw-back and penalties will be announced by the Government later). If fraud is involved, the employer may consider committing a criminal offence and if convicted, may subject to imprisonment.

5. Taxability of subsidy received

The subsidy received by enterprises and individuals is exempted from Hong Kong Profits Tax/Salaries Tax.

We will continue monitoring the status about the application of subsidy under ESS and will provide you with updates as soon as latest information is available.

In the meantime, please feel free to contact us to find out how we can assist you in respect of the above relief measures.