.jpg.aspx?width=600&height=399)

How does IFRS 9 impact your Bank?

Slightly more than two years after the International Accounting Standards Board decided to replace IAS39 with IFRS 9 which came into effective from 1 Jan 2018, many banks had reported significant changes to their financial reporting and lending behavior. As under IFRS 9, banks are required to recognise the credit loss allowance of the financial assets much earlier compare to IAS 39 which impairment is generally recognised only when a credit loss event has occurred.

The introduction of IFRS 9 comes with the intention to promote financial assets to be measured at fair value recognised in profit and loss (FVPL), unless criteria are met for classifying and measuring the assets at either amortised cost (AC) or fair value through other comprehensive income (FVOCI). As a result, the classification of banks’ financial assets, including loans, equity investment, bond and receivables are impacted. Banks will have to start making provision for possible future credit losses in their very first reporting after the loan is granted, even though it is highly unlikely that the loan will turn into defaulted. As a result, we are seeing some changes of lending behavior to avoid the volatility of income statement.

Let us recap what are the key components of IFRS 9. Essentially, it contains three main topics: i) classification and measurement of financial instruments, ii) impairment of financial assets and iii) hedge accounting.

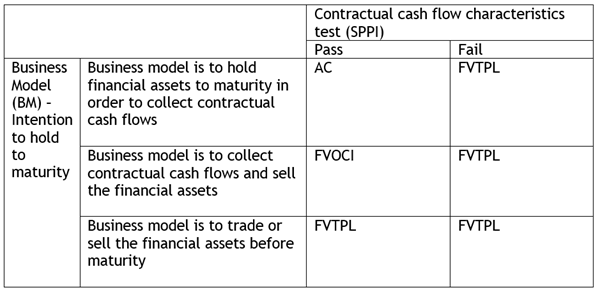

i) Classification and measurement of financial instruments

Under IFRS9, the classification & measurement requirements for financial assets have been revised. The assets will have to go through the business model (BM) and the solely payments of principal and interest (SPPI) tests as follow:

While the above matrices look quite straight forward, the actual tests often require a closer examination of the financial assets and the contractual terms. More than often if the contractual cash flow or interest cannot reflect the consideration of time value of money and for the credit risk related to the instruments, it will fail the SPPI test.

Take loans for example. One will expect that loans should be quite straight forward and be measured at AC. However, in many instances, Banks may decide to sell part of their loan portfolios and lend more complex loans which will result in failing the BM & SPPI tests. This is especially so when the loans contain features like inverse floating rate, conversion option, leveraged interest rate, linking to the value of the equity of the issuer, the reference rates that are not dominated in loan's currency, etc.

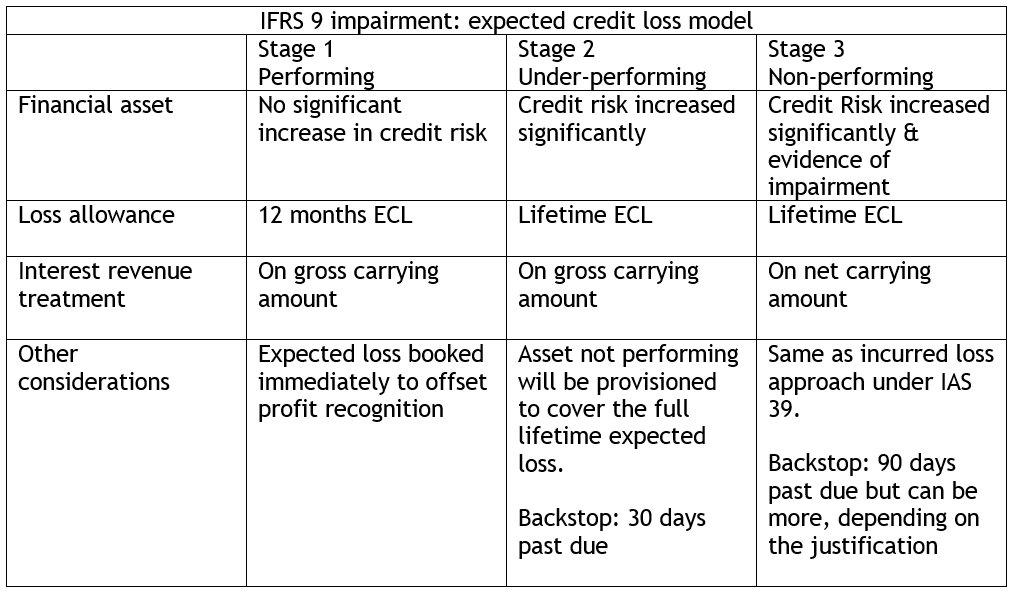

ii) Impairment of financial assets

Under IFRS 9, it requires assets impairment to be measured at expected credit loss (ECL) model include forward looking information instead of incurred loss model under IAS 39. The ECL can calculate by probability of default (PD) x loss given default (LGD) x exposure at default (EAD).

Impairment will be measured either at:

- Stage 1 > 12 months ECL for performing assets, or

- Stage 2 > Lifetime ECL for assets of which credit risk increased significantly, or

- Stage 3 > Lifetime ECL for those impaired assets.

Assessment on whether there has been significant increase in credit risk since initial recognition which result in transfer from stage 1 to stage 2 should be made at each reporting date.

'Simplified approach'

IFRS 9 allows banks to apply a simplified approach for trade and lease receivables that do not contain a significant financing component. In simple terms, a lifetime ELC under simplified approach is based on the historical loss rate (normally based on two to five years data) multiply the gross balance of group of similar receivables in different age-buckets.

Bank should also pay attention to the treatment of guarantee under IFRS 9. When the bank issued a financial guarantee, the guarantee premium will be recognsed as financial liability or 'deferred revenue' at their fair value at the initial booking, and subsequently measured at the higher of i) the amount of ECL as measured under IFRS 9; or ii) the amount initially recognised less, when appropriate, cumulative amortisation. As a result, the financial guarantee business become less attractive in view that the ECL may be higher than the premiums received due to the stricter requirements under IFRS 9.

iii) Hedge accounting

IFRS 9 updated the guidelines for hedge accounting to enable banks to reflect better hedging activities in their financial statements. The changes have broadened the hedging instruments to include non-derivatives instruments (like shares in commodity linked funds or debt securities) measured at FVTPL. IFRS 9 allows partial hedge of risk component of non-financial items rather than the entirety under the IAS39. The hedge effectiveness test of 80%-125% under IAS39 has also been replaced by the principle-based criteria such as the economic relationship between the hedge instruments and the hedge items.

While IFRS 9 allows the rebalancing of the hedge without the need to terminate the current hedging, it does not allow voluntary termination of the hedge unless the risk management objectives have changed, or the hedge has expired or no longer eligible.

The disclosures related to the hedges accounting under IFRS 9 have also been strengthened to include the requirements to disclose risk management strategy, impact to the future cash flow and the financial performance.